Kotak Mahindra bank my family savings account is specially made for the families. It brings the entire family under one account. It allows every family member to access the various benefits and facilities of the savings account. However, there is a minimum balance requirement, and…

SBI made money payment transactions easier with Internet Banking facility for its users. To avail the SBI Internet Banking facility, first-time customers should enter online login credentials provided in SBI’s Internet Banking Kit. SBI also allows users to change their username and password for later…

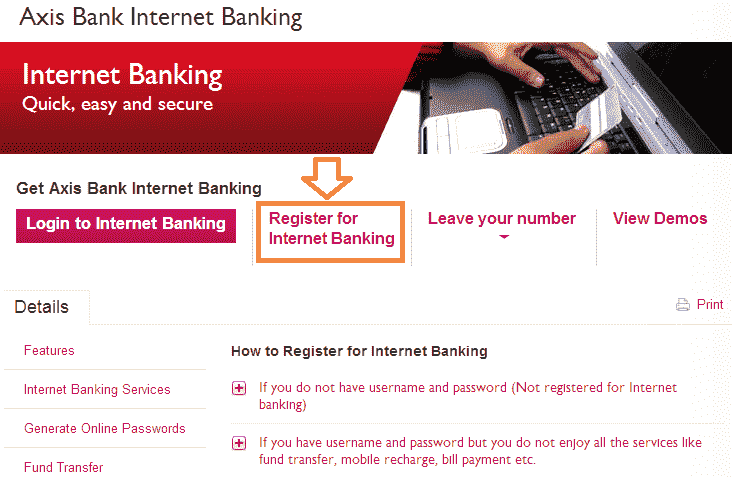

Activate Axis Bank Internet Banking: Traditional banking has become a thing of the past these days, in fact, a lot of banks these days offer banking services over the internet. There used to be a time where you would have to participate in long queues…

Net banking is one of the essential and high-handed amenities that brought suited options of banking for the account proprietors—the Indian Banking sector at a gallop trailblazing with the inception of assorted innovatory banking courses of action. If you have an account with Tamilnad Mercantile…

In today’s world, most banks offer the option of online banking. Through this option, you have loads of advantages. Not only are you able to pay your bills online, but you can also transfer money between accounts. More to add, you can also access the…

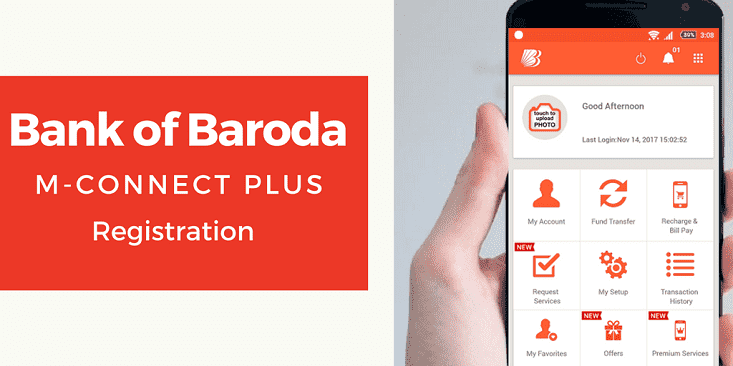

Bank of Baroda is one of the popular public sector banks in the country. It has launched the best mobile banking application for the smartphone users. M-Connect Plus is the Baroda mobile banking app. It enables the users to transfer funds, check balance, view balance,…

No matter what kind of financial difficulties you run into in life, selling your home is always an option to get you out of them. With a robust real estate market driving high home values all over the UK, even small residences can net you…

Our country is going digital now. After the 2016 demonetization, most of the things are changing in our country. Likewise, people started using digital payments at shops, places, shopping malls and reduced the usage of cash. It is all under the concept and initiative of…

Bank of Baroda is one of the popular banks in India. It offers all the services that a customer required in their banking assistance. For example, 24/7 customer care service, savings bank account, current bank account, loan, credit cards, and much more. It can be…